6 Tips For Managing Money As A Couple

One of the leading causes of arguments between couples and spouses is finances. Learning the art of managing money as a couple is vital for a relationship.

One of the leading causes of arguments between couples and spouses is finances. Learning the art of managing money as a couple is vital for a relationship.

Many couples today seem to struggle with the for richer or for poorer aspect of vows, especially when you find yourself on the poorer end of the stick.

Some couples have separate bank accounts and don’t share their money, while others have a joint account. When you are not honest about spending money, or are overspending, it can cause serious troubles in a marriage or relationship.

6 Tips for Managing Money As A Couple

Below are some tips for you to help manage money as a couple, and not struggle the way many relationships do.

You can decide if any of these will work for you and your partner, and find the best money management solution for you.

Separate Accounts

Having separate accounts in a relationship is a must for me, and many couples.

For me, this stems from being in a relationship where I was dependent on my partner. He was also horrible with his money management skills.

We separated, I became a single mom, and I stayed single for many years.

Those experiences made managing my own income very important to me.

Having separate accounts can help:

- Make sure you each have your own amount of money

- You know how much goes towards your bills and debt

- Put you in charge of how much money you can spend on whatever you want once you have taken care of your responsibilities

When you have separate accounts you each have a bit more control over your own personal finances.

For couples who have separate accounts, you need to make sure you communicate with your partner about the household finances. This ensures you know who is paying for what so bills don’t get left unpaid.

In my relationship, my partner pays a larger portion of our rent. He also is responsible for the cable, internet, and his phone bill.

Each month I transfer my portion of the rent over to him since that bill comes out of his account. Then from my account, I pay for the hydro, gas, water, and my phone bill.

For groceries and other things we need, we generally just buy what we need when we need it. While I often do the big grocery shops, he will often pick up things we have run out of before grocery day.

Even with having separate accounts you will still have to budget, but it can help relieve stress for some.

Having separate accounts won’t work for everyone, but this has been a relationship game changer (in a good way) for many people I know!

Long Term Goals

Relationship experts don’t lie when they say communication in a relationship is key. When managing money as a couple, communication is imperative.

As a couple you need to sit down and discuss any long-term goals you might have.

Maybe you want to paint your home or your appliances need replacing soon. Or do you want to retire at a certain age? Perhaps a baby is in the near future?

All of these take time and dedication to saving in order to make them happen.

Life is busy for everyone, but it is important to sit down as a couple and create a savings plan. Discuss how much money you want or need to save every month towards your long-term goals. Then you can decided how much each of you will contribute to that total savings amount.

Last but not least, re-evaluate your goals every few months to ensure you are on track to meet them.

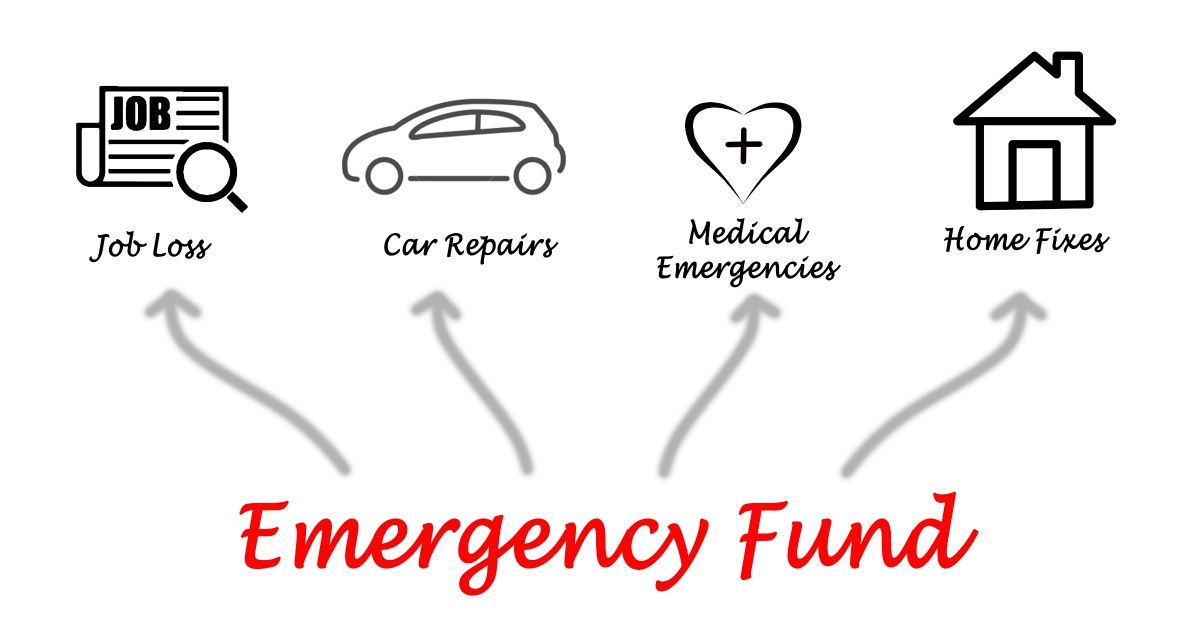

Emergency Fund

I cannot stress enough how important it is to have an emergency fund. Whether you are a single parent or a couple, having money to fall back on in the case of an emergency can truly relieve a lot of stress.

In 2013 when we had the ice-storm and were without power for 5 days we lost all of our food. I am talking two fridges with freezers and a deep freezer full as I had just done a big grocery shop the week before.

Top that unexpected cost of replacing all of our food with going into pre-term labour with Bella. She was not due until February and I gave birth to her one day after we regained power from the ice storm. She had to stay in NICU for 17 days, and as you can imagine the costs of her early arrival piled up quickly.

- Hospital parking fees

- Cab fare

- All of the things we still needed to buy for her like a crib mattress, bedding, bottles, and so on

Thankfully after losing my home as a single mom due to having no savings and losing the job I had, I learned my lesson and have always had a hefty savings account to fall back on. Had I not had that savings to fall back on, we could have been in a bad financial position that year.

Emergencies that can strain ones finances usually come out of nowhere and can put a great deal of stress on you. You never know when one of you could lose your job, the furnace breaks mid-winter, unexpected home repairs pop up, and so on.

I suggest working towards saving enough money for 3 to 6 months of your household expenses, that way if you have no income you can still cover your bills, or if another unexpected emergency arises you have money to cover the costs. Doing this will help bring financial security and protection for your family.

Debt

Staying out of debt is a big deal for me. I don’t like owing money and rarely use my credit card.

Actually, the only times I use my credit card are in an emergency, and to build up my credit by buying things I have the money for. I always make sure to pay those immediately off of the card so I don’t pay interest fees.

If you have debt make sure you put money toward your bills that are needing to be paid off each month. Even if it is $25,it is something, and slowly but surely you can work towards becoming debt free.

If you are already in debt, try not to go further into debt.

- Stop using credit cards

- Live within your means

- Create a second stream of income

- Track your spending so you can see where you can make changes

- Trim down your luxuries to afford your necessities

- BUDGET BUDGET BUDGET

Big Ticket Items

There are times when purchases should be discussed and agreed upon between couples, and times where it is not necessary.

If you are planning to make a big purchase, make sure you talk it over with your partner.

Create a spending amount that any item that is x amount of dollars or more, you have to call the other person to discuss it.

Doing this will ensure you both don’t impulse shop or spend a ton of money, not knowing what the other partner has spent. Getting into this habit will help keep each of you accountable and protect you from overspending on an item.

A good example of this could be if one partner is a free spender and the other is good at getting/finding deals. By discussing this big purchase, the saver may know of a way to get that item for less than what the free spender would have paid. That money saved can then be put towards something else, like retirement savings!

Fun Money

One thing I don’t do in my relationship is parent my partner. This can lead to your partner hiding their spending which can lead to much bigger issues.

Steve has his hobbies like riding his bicycle, or his yearly trip with the boys that he puts his money towards.

For me, so long as his bills are paid and his other financial responsibilities taken care of, I don’t feel the need to dictate or interrogate his spending.

Having fun money that you can do what you want with, without worry of your partners opinion can ease financial tension.

Sit down and decide on an amount of money that you can each have to spend as you wish. Whether it be $20, $50, or $100 each that you can afford to do whatever you want with.

The money you allot as fun money can be used however you like. Maybe it’s a night out on the town with the girls, or that pair of heels you have been eyeing. This fun money offers a little freedom, and you don’t feel you have to ask to use it.

BUT, only do this if you have the extra money and it won’t hinder paying the bills, or paying down debts.

Do you have any other tips on managing finances as a couple that work in your relationship?

- Printable Kids Summer Bucket List - June 4, 2025

- Save On Summer Family Fun - June 4, 2025

- Homemade Strawberry Lemonade Popsicles - June 3, 2025

Leave a Reply